AS Deloitte Audit Eesti, in Tallinn, Estonia, provides audit services to Bondora. AS Deloitte Audit Eesti are chartered accountants, members of the Estonian Board of Auditors in the Republic of Estonia, and qualified to practice as auditors in the Republic of Estonia.

Bondora had its 2014 and 2015 annual reports audited by Deloitte. The audits were carried out according to IFRS and were issued with an unqualified opinion in both years.

Erki Mägi, of AS PricewaterhouseCoopers, in Tallinn, Estonia has been named as Bondora’s internal auditor, reporting to the Supervisory Board. Erki Mägi is a certified internal auditor and qualified to practice as an internal auditor in the Republic of Estonia.

To date, AS PricewaterhouseCoopers has performed one full-scale review of Bondora’s internal processes and controls and will continue to undertake regular independent assessments of Bondora´s processes. The aim of such audits is to assess whether Bondora, its management and staff members’ activities comply with applicable legal requirements, Estonian Financial Supervision Authority rules, the Company’s internal rules, the Management Board’s and Supervisory Board’s decisions, and Bondora’s contractual agreements with third parties, and whether these activities are in accordance with industry best practices.

Rein Ojavere, Bondora’s Chief Financial Officer, is responsible for overseeing financial planning and control, tax, accounting, audit and shareholder relations, including reporting.

BOARD STRUCTURE

Bondora’s articles of association set out a two-tier management structure consisting of the Supervisory Board and the Management Board. Briefly speaking, the Supervisory Board’s role is to supervise certain activities of the Management Board in the best interests of Bondora and its shareholders; the Management Board’s role is to serve as the executive body of Bondora, with the authority to manage the business.

MANAGEMENT BOARD

Bondora is managed by the Management Board. As of the date of this Memorandum, the Management Board is comprised of two members, Pärtel Tomberg and Rein Ojavere. The details are set out below.

Pärtel Tomberg (Chief Executive Officer)

Pärtel Tomberg is the founder and CEO of Bondora AS. Mr. Tomberg has transformed Bondora into a leading pan-European marketplace lender from a dorm room startup he founded in 2008. He has helped Bondora establish a new standard in marketplace lending by being first in a number of areas:

- first marketplace open to investors across Europe;

- first marketplace providing credit seamlessly across multiple countries;

- first rating system designed to allow loans originated is different markets to be comparable;

- first marketplace open to accredited investors globally; and

- first marketplace in Europe with a public API and granular performance data.

Mr. Tomberg was previously a member of the Nordic, CEE and Baltic region management teams of Quelle AG and, subsequent to that, Halens AB. Both companies sold fashion bundled with up to a 36-month installment plan, placing them among the largest non-bank consumer lenders in their target markets. He graduated summa cum laude from the Oxford Brookes University with a BA.

In addition to the directorship roles described above, Mr. Tomberg holds or has held the directorships (or, in certain cases, what were once members of partnerships) detailed in the table below, at some time during or over the past five years.

| Current directorships/partnerships |

Past directorships/partnerships |

| Member of the management board: Bondora AS (chairman), Bondora AS, Bondora Capital OÜ, Bondora Servicer OÜ, Tomberg Management & Consulting Group OÜ, Social Developments OÜ |

Member of the management board: Elektrooniline Vahekohus OÜ |

Rein Ojavere (Chief Financial Officer)

Rein Ojavere is the CFO of Bondora AS and is responsible for all of its financial matters, from investor relations to internal financial management.

Mr. Ojavere is a seasoned finance and investment professional. He was previously Head of Corporate Banking and a board member at DNB Bank in Estonia; Partner and Head of Research at asset management company Northern Star (formerly Limestone Investment Management); and Fund Manager and Head of Research of Hansa Investment Funds. He has also held several investment banking positions at Suprema. Mr. Ojavere holds a master’s degree in economics and business administration from the University of Tartu and is a CFA charterholder.

In addition to the directorship roles described above, Mr. Ojavere holds or has held the directorships (or, in certain cases, what were once members of partnerships) detailed in the table below, at some time or over the past five years.

| Current directorships/partnerships |

Past directorships/partnerships |

| Member of the management board: Bondora AS, Bondora Capital OÜ, Bondora Servicer OÜ |

Member of the management board: DNB Pank, OÜ Front Consulting, OÜ Limestone Partners, OÜ Limestone Advisors.

Member of the supervisory board: AS Limestone Investment Management. Director: Limestone Opportunities Fund S.A. |

MANAGEMENT BOARD RESPONSIBILITIES

The Management Board is responsible for representing Bondora and directing its daily activities in accordance with the strategy set out by the Supervisory Board and Bondora’s articles of association. The Management Board also controls the daily activities of Bondora employees. The Management Board has a joint representative right: transactions must be approved by two members, one of whom must be Pärtel Tomberg.

Members of the Management Board adopt resolutions at board meetings. Such meetings are considered to have a quorum if over half of the members take part. Resolutions are adopted if a majority of the votes of all Management Board members are in favor. Each member has one vote; in the case of a tie, the Chairman of the Management Board casts the deciding vote. Management Board meetings may be held through electronic means, provided that all members participating in the meeting can hear and communicate with other participating members.

The Management Board is also responsible for creating and presenting the following at the general meeting in accordance with applicable law: the management report; the annual report, together with its appendices the auditor’s report; and the profit distribution proposal.

As of date, 100% of Bondora’s issued shares are fully paid and duly registered. The holders of the shares are entitled to receive the remaining profits, if any, as declared from time to time in accordance with Bondora´s articles of association. They are also entitled to one vote per share at Bondora’s general meetings; however, the shares are divided into three classes, with each having somewhat different rights. Moreover, as a shareholder of Bondora, the subsidiary of Valinor Management LLC has certain specific rights that are prescribed in the articles of association, including, for example, veto rights over a limited number of shareholders’ resolutions. Bondora’s share register is maintained and held by the ECRS.

The general meeting of shareholders is Bondora’s highest governance body. An annual shareholders’ meeting must be held every year; an extraordinary shareholders’ meeting may be called by the Supervisory Board on its own initiative or at the request of the Supervisory Board or shareholders holding in aggregate not less than 5% of Bondora’s share capital. Each Bondora share carries the right to cast one vote at any shareholders’ meeting.

Bondora Supervisory Board

SUPERVISORY BOARD STRUCTURE

In accordance with Bondora´s articles of association, the Supervisory Board, which oversees the Management Board, is currently comprised of three directors who were appointed at a general meeting of shareholders. Joao Monteiro, Mati Otsmaa and Phil Austern. The details are set out below.

Joao Monteiro (Chairman of the Supervisory Board)

Joao Monteiro is an international manager with a primary focus on strategic repositioning and restructuring of business operations and supply chains. He is Head of Global Business Development of Contract Logistics at Kuehne+Nagel. Previously, he was involved in organizational development at LSG Sky Chefs as well as Roland Berger, the leading European management consulting firm. Mr. Monteiro holds an AMP certification from the Harvard Business School.

In addition to the directorship roles described above, Mr. Monteiro holds or has held the directorships (or, in certain cases, what were once members of partnerships) detailed in the table below, at some time during or over the last five years.

| Current directorships/partnerships |

Past directorships/partnerships |

| Member of the management board: Mosaic Capital Partners Ltd Chairman of the Supervisory Board: Bondora AS |

|

Mati Otsmaa (Supervisory Board Member)

Mati Otsmaa is a C-level management executive from San Francisco with extensive experience in building e-commerce and financial service businesses. He has worked in a senior marketing capacity internationally, with focus on consumer credit lending, for American Express, Barclays, Citibank, Chase, Experian, HSBC, Hyundai and Providian. Mr. Otsmaa has an MBA from the University of Southern California.

In addition to the directorship roles described above, Mr. Otsmaa holds or has held the directorships (or, in certain cases, what were once members of partnerships) detailed in the table below, at some time during or over the last pive years.

| Current directorships/partnerships |

Past directorships/partnerships |

| Director: Market Direct Inc. Member of the Supervisory Board: Bondora AS |

Director: AffiniCorp Inc. |

Phil Austern (Supervisory Board Member)

Phil Austern is a Partner and founding member of Valinor Management LLC. Prior to that, he was an analyst at Bridger Capital. From 2005 to 2006, Mr. Austern was a vice president at Francisco Partners and a member of the team that launched the firm’s London office; from 2000 to 2003, he was an Associate at the firm. Earlier in his career, Mr. Austern was an analyst at DLJ Merchant Banking Partners, the leveraged buyout arm of Donaldson, Lufkin & Jenrette.

Mr. Austern graduated cum laude from New York University’s Stern School of Business with a BS in finance and economics and received in 1998 and earned an MBA from the Wharton School of the University of Pennsylvania in 2005.

In addition to the directorship roles explained above, Mr. Austern holds or has held the directorships (or, in certain cases, what were once members of partnerships) detailed in the table below, at some time or over the last five years.

| Current directorships/partnerships |

Past directorships/partnerships |

| Member of the Supervisory Board: Bondora AS |

|

SUPERVISORY BOARD RESPONSIBILITIES

The Supervisory Board is responsible for planning Bondora’s business activities, organizing the management of Bondora, supervising the activities of the Management Board and making decisions as stipulated by applicable law and in Bondora’s articles of association. In addition, the Supervisory Board has such functions and competencies as are provided for in Bondora’s articles of association and by applicable law.

Meetings of the Supervisory Board are held whenever necessary, but not less than once every three months. The Supervisory Board has the right to adopt resolutions without calling a meeting if all members consent to it.

The following measures and/or transactions require a ratifying decision by the Supervisory Board, which, to be valid, must have (i) the approval of a majority of its members and (ii) the approval of the member of the Supervisory Board appointed by the subsidiary of Valinor Management LLC:

- adopt and/or change the strategy/business plan and the budget;

- appoint and/or dismiss the CEO and/or chairman of the Management Board;

- approve any material transactions (including, but not limited to, acquisitions and the issuance of debt) not previously included or provided for in the approved budget;

- approve any asset disposal with a monetary value in excess of EUR 50,000;

- initiate or settle, including by way of compromise, any legal proceedings outside of the ordinary course of business where there are claims with a monetary value in excess of EUR 50,000;

- make a material tax election or alteration of the tax status of Bondora other than as required by changes in law, regulations or accounting principles;

- enter into any related-party transactions, other than in the ordinary course of business and on an arm’s-length basis;

- increase the annual compensation of any employee making in excess of EUR 75,000 by more than 10%;

- enter into any contracts with a monetary value of more than EUR 50,000 not previously included or provided for in the approved budget;

- enter into employment, service, consultation or cooperation agreements with an annual monetary value of more than EUR 50,000 not previously included or provided for in the approved budget;

- authorize or grant participation in an equity incentive or similar participation program, including any option pool.

It should be noted that the Supervisory Board confirms the strategy/business plan and the budget in writing for a year and reviews updates quarterly as it sees fit.

How to start investing on Bondora?

To start investing on Bondora:

- Open an investor account

- Fill out the identification form

- Choose your strategy for the Portfolio Manager

- Add funds to your account and start investing

When you have activated the Portfolio Manager it will immediately start searching for loans that fit your selected strategy. The starting bid size is €5 which will double after every 200 unique investments. You can also set a custom bid size to override the automatic bid size set by the Portfolio Manager.

What kind of documents do accredited investors need to provide?

If you are an accredited investor based on your net worth we ask you to send us bank statements, brokerage statements, other statements of securities holdings, certificates of deposit and/or tax assessments and appraisal reports issued by third parties in order to verify assets, a consumer report from at least one of the nationwide consumer reporting agencies to verify liabilities and also a written confirmation that all liabilities necessary to make a net worth determination have been disclosed (all information provided may not be more than 3 months old).

If you are an accredited investor based on your income we ask you to send us tax forms that report revenue (for example in US: W-2, Form 1099, Schedule K-1 or filed Form 1040) for the last two years and also a written confirmation that you have reasonable expectation of reaching the same income level in the current year.

You don’t need to provide above-mentioned documents if you send us written confirmation from a broker-dealer, a registered investment advisor, a licensed attorney or a CPA that you have taken reasonable steps to verify that you are an accredited investor within the prior 3 months and that it was determined that you are an accredited investor.

Provided that all necessary information have been sent we will review the documentation within 5 business days. In case of successful verification you can start investing via our platform.

Who can invest on Bondora?

Anyone over the age of 18 living in the European Union, Switzerland or Norway and businesses registered in the EU or from any other country approved by Bondora. If you are an investor from Australia, Brazil, Canada, Hong Kong, India, Japan, South Korea, Mexico, Singapore, South Africa or The United States of America then we need to verify that you are an “accredited investor”. As part of the verification process we ask you to send us different information and documents.

How much time do ivestors need to spend on investment management?

PASSIVE INVESTORS

If you have little free time to spend on your investments and are expecting to earn the market’s average return rates, you can automate your investments with our Portfolio Manager. All you need to do is select your preferred strategy (from Ultra Conservative to Opportunistic) on the Portfolio Manager settings and add funds to your Bondora account and let the Portfolio Manager do the rest, including reinvesting repayments from your investments, thus saving you time and increasing the likelihood of your money getting invested as quickly as possible.

ACTIVE INVESTORS

If you want to take a more active approach to your Bondora investments, then you get programmatic access to the loan listings to make investments using the API. The API is accessible on live site at https://api.bondora.com/. If you are interested in learning more about the API, please send us an email to api@bondora.com

What is Portfolio Manager?

You can use Portfolio Manager to automate the investment process. In order to set up or edit your Portfolio Manager you need to navigate to Dashboard, scroll down and choose your preferred strategy and settings, click Activate Portfolio Manager button and agree to its terms and conditions (Portfolio Manager agreement).

Features:

- Investment size calculation tailored to meet your targets

- Advanced settings that let you over-ride each individual variable in our investment size formula

- Option to split your investment into multiple smaller bids to make it more liquid

- Control through granular risk-return strategy options

- More inventory as Portfolio Manager will be also buying from the Secondary Market

Investment size calculation

The suggested investment size calculation takes into data specific to your portfolio and strategy to arrive at the suggested investment size. The algorithm includes six variables: (1) point of diversification (X – by default 200); (2) the desired capital deployment period (Y – by default 2 weeks); (3) the number of loans expected to be available for investment over this period (Z); (4) your total deposits (T); (5) your available cash balance (C); and (6) your expected cash inflow over the defined deployment period (CF).

The suggested investment size is calculated by dividing your cash balance and expected cash inflow over the defined deployment period with the number of loans expected to be available during this period. In simple terms the suggested investment size equals (C + CF) / Z. The minimum investment is 5 EUR. The maximum investment is calculated by dividing your total deposits with point of diversification (T / X). Point of diversification is the number of loans that you should include in your portfolio to have a reasonably diversified portfolio.

Advanced settings that let you over-ride each individual variable in our investment size formula

Investors who feel that the default settings do not suit them can override most of the individual variables in the formula above. You can override point of diversification and capital deployment period. You can of course set your own minimum and maximum amounts instead of using our formula. Additionally you are able to define the free cash balance you would like to keep on your account for withdrawals.

Option to split your investment into multiple smaller bids to make it more liquid

Investors on Bondora are not all investing with the same amounts of capital. Therefore some investors are making considerably larger investments into single loans compared to others. We have an option to split your investments into smaller bids in order for larger investors to be better able to liquidate parts of their portfolios. In case your investment per loan is 100 EUR and you have defined the bid size to be 15 EUR then the system will make 7 bids into a loan, 6 bids of 15 EUR and 1 bid of 10 EUR.

Control through granular risk-return strategy options

Investors looking to increase or decrease the available investment pool will be able to do so by choosing among 9 strategies. We are adding Ultra Conservative as well as Opportunistic strategies as well as options in between the 2 new and 3 existing strategies.

Please remember that these strategies remain within the context of Bondora and therefore an Ultra Conservative strategy cannot be compared with an ultra-conservative stock or bond strategy (e.g. blue chips or German bonds). Bondora should be viewed as higher yield part of your portfolio and total portfolio allocation towards Bondora should be set based on this assumption.

Expected portfolio distribution charts include existing loans to improve estimates

The expected portfolio distribution charts calculation includes both your existing and new loans. The loans that are expected to be added to your portfolio over the desired allocation period are added to the existing portfolio to arrive at the estimates. The estimates for new loans are calculated based on your chosen risk-return strategy and recent market statistics.

Portfolio Manager will be also buying from the Secondary Market

We have been steady increases in secondary trading since we introduced our API. However the trading still considerably lags behind Primary Market volumes and available inventory as most investors are not using the Secondary Market. We are addressing the liquidity constrain by adding Secondary Market inventory to the pool available for the Portfolio Manager. This step will both increase the liquidity for existing investors as well as allows new investors to buy into seasoned and lower risk assets.

The Portfolio Manager will buy only loans that are not overdue (principal nor interest) at a price equal to the principal balance or below. No trades will be made above par or on overdue loans until it’s possible to completely harmonize the Primary and Secondary Market pricing.

In case you are interested only in new originations then you can turn off this option through the Portfolio Manager Advanced Settings.

Bondora API supports the more active, trader type of investors by allowing granular reporting and customized investment strategies. It gives active investors the flexibility that the Portfolio Manager does not. API is an interface for accessing the functionality of Bondora platform without the user interface (UI). Bondora API provides information and exposes Bondora’s functionality for other services and applications. Investors benefit from the API by having access to data and services that cater to their individual wishes and by getting the ability to bid on specific loans that fit their personal investment strategy. Investors can use Bondora API in common programming languages.

Recommended starting amount?

Bondora generally do not make any recommendations but they have seen that investors generate a more stable return when they diversify their investment across many different loans. It is also best practice to keep your investments continually active and systematically add funds to reach your investment goals. Bondora return models are built on an assumption of a portfolio having minimum of 200 unique investment with equal exposure.

Why is it wise to have a minimum allocation of 200 loans and €1000 for your portfolio?

The minimum bid size is €5. The bid size is doubled after each time your portfolio increases by 200 loans. Or you can use our “Bid Size” feature that enables to set your own bid size to any amount as long as it is divisible by 5. 200 is an important number because analysis of the investors’ portfolios shows that the risks of a portfolio substantially decrease after reaching 200 unique loans. This means that your portfolio return becomes stable and on 91% of cases is above 10% of return. Therefore increasing the size of the investments after each 200 new loans allows you to lend your money faster without increasing risks.

Can I liquidate my portfolio before final loan deadline?

Yes, Bondora has an active Secondary Market for selling loans with discount or mark-up.

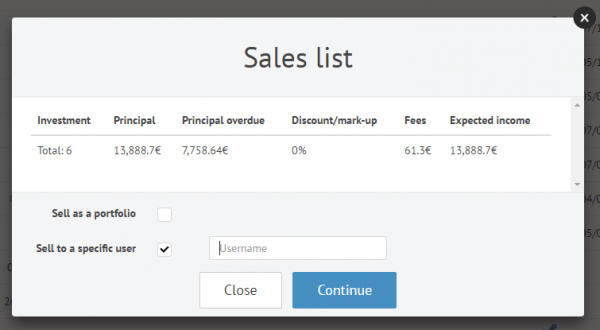

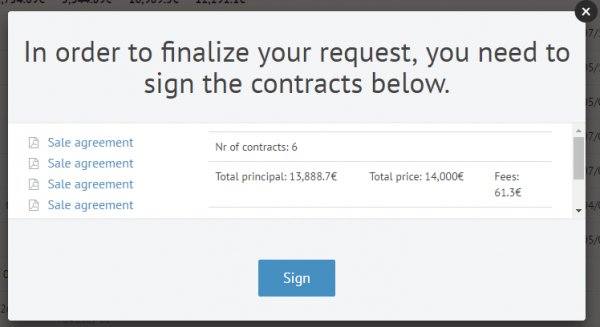

Selling investments manually on Secondary Market

To sell your investments on Secondary Market log in with your Bondora credentials to see an overview of your investments on Invesments page. Choose the loans which you would like to sell by clicking on cart icons. When finished picking the loans and adjusments are made confirm the selling from Sell all button and the loans will be put on sale.

Faster liquidity with one-click sell button

Selling your investments is made extremely easy. You will be able to define the amount of capital you need and the system will do the rest. This feature is neatly packaged on the Dashboard. Loans will be put on sale with current loans first and overdue ones thereafter with newest loans sold first before seasoned ones. The sale price will be calculated as the principal balance less principal payments overdue by schedule. In other words if you put your entire portfolio to sale then it will be priced the same way as the account value is calculated.

How does Bondora safeguard my money?

The money borrowers and lenders transfer to Bondora is held on a segregated client account. No interest shall be paid for money held on the client account. We bank with SEB Bank, one of the largest banking groups in Scandinavia. You can find additional information about their credit ratings on SEB Group’s home page.

The money transferred to Bondora may only be used pursuant to Terms of Use and for performing the obligations of the loan agreements. The respective amount in the bank is by its nature a claim (against the bank) that Bondora has acquired in its name but on behalf of the customer and only with the purpose of using it for performance of the mandate. Therefore the respective money does not belong to the bankruptcy assets of Bondora and a claim for payment cannot be made for the money in enforcement proceedings, and it shall likewise not be reflected in the balance sheet of Bondora. This above all means that by transferring money to Bondora you do not completely transfer it to the assets of Bondora but instead retain the necessary rights concerning the money in order to recover it fully in case of financial troubles of Bondora.

All payments made to the Bondora account shall be reflected as receipts on your client account. You will receive an email notifying you of an arrived deposit or a repayment. Bondora keeps records and accounts of every payment to and from Bondora account as well as payments between different customers. A daily internal and external reconciliations are made to ensure the accuracy of the records and accounts.

You have the right to withdraw your funds to an account in your name that you have used to make payments to Bondora account. You need to verify all withdrawals using two-factor authentication. All withdrawals will further be reviewed by our accounting team before submitting to our bank over a secure electronic payment order.

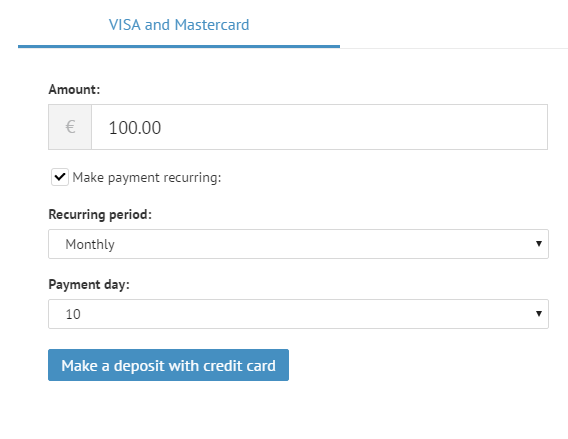

How can I add funds/deposit to my Bondora account?

ADDING FUNDS FROM WITHIN THE EUROZONE

You can add funds to your Bondora account either through a SEPA bank transfer or through third party services such as TransferWise, Currencyfair and EVP International. As Estonia is within the Eurozone, please make sure you specify that the payment is to be made in euro when initiating the payment through your internet bank or a local branch.

The SEPA payments take a maximum of 3 business days to arrive and the costs are generally the same as for domestic payments for the Eurozone customers. However, please make sure to verify this with your local bank before making the payment. In case your bank also levies a charge on the receiver of the payment, then these charges will be passed onto your Bondora account.

All details required for making the payment can be found on your Dashboard when clicking on ADD FUNDS tab after you have completed the initial identification process. Please note that withdrawals are only possible to the same account from which the funds were transferred and currently only a single bank account can be tied to your Bondora account. These steps are required to ensure that your funds are not compromised even in case someone manages to get hold of your Bondora account access details.

ADDING FUNDS FROM OUTSIDE THE EUROZONE

TransferWise is useful when making payments outside the Eurozone allowing you to save money and time. If you use a third party service provider such as TransferWise, Currencyfair and EVP International to add funds to your Bondora account for the first time we require some additional information to verify your account before you can start investing.

Please send us proof of your personal bank account details to investor@bondora.com. This can be an account statement or screenshot of your personal online banking page, which would cover the following information:

- Bank account IBAN

- Bank BIC/SWIFT code

- Your name

- Bank name

We are only able to verify your bank account as soon as we receive the mentioned information above. Please note, that you will not be able to withdraw funds until your account is fully identified. Please note that transfers through TransferWise may take up to 5 business days to receive.

How do I withdraw funds from my account?

If you are making a WITHDRAW request for the first time then we need to fully identify your account before you can withdraw money from your Bondora account.

The identification process is required for ensuring safety of your personal information and simplification of money withdrawal process. Please go to your settings page on the top right corner link and complete the missing steps. Once your identity and address has been verified, please follow the guidelines below to withdraw money.

- Go to your Dashboard

- Click Withdraw funds and insert the amount you would like to take out from your Bondora account and click “Withdraw”

Can I also withdraw funds using TransferWise?

Yes, TransferWise withdrawals are made easy through the Dashboard.

Our customers outside of Eurozone or who do not have a euro account can now easily withdraw money through Transferwise. Simply enter the withdrawal amount, choose your currency and use the Transferwise option. Transfers through TransferWise may take up to 7 business days. Everything else will happen automatically.

PS! Please notice that TransferWise service can be used only for cross-currency payments, EUR to EUR transactions are not supported. Please also make sure that your bank accepts TransferWise payments.

What performance reports are available to investors?

You will be able to download on-demand performance reports for freely chosen periods that cover:

- Investments dataset: Performance data on every loan in your portfolio

- Portfolio Cash Flow, P&L Statement and Balance Sheet: Allows you to see the total portfolio cash flow, P&L and Balance Sheet as of the end of each month.

- Historic payments: Includes all received payments in euro, categorized by payment type, date and loan ID.

- Secondary market transactions history: Includes all of your transactions on the Secondary Market.

- Future cash flows: Includes all scheduled payments in euro, categories by payment type, date and loan ID.

The data is available for your portfolio as well as for all loans issued on Bondora that you can use as a benchmark.

In our dataset updates in the past year we have consolidated all our different data sources and thereby made the exact same data and information available to each investor regardless of the channel they use.

Today there are differences in available data points as well as the definitions behind different data points with similar labels. These differences are due to having our technology built over 7 years. Therefore we need to consolidate the data sources through a new technology that will allow us to resolve all data conflicts and discrepancies. Shortly it will be very easy to navigate in the vast sets of information Bondora makes available.

You can keep track of the changes through our data map available on the Public Reports page. This map shows which data points are available through which channels, the label in Data Export as well as the description. We have also included the previous label if there has been a change (highlighted in italic). Descriptions of removed data points are all set to [OBSOLETE].

Cells marked in green indicate that this data point is already available in the particular channel whilst yellow means that it’s going to be released shortly. Most white cells will soon also be colored green. This is unless the particular data point is not available at the time of the data source in question is polled (e.g. it is not possible to show loans active late category when it is still on the Primary Market).

Please note that there might still be label changes in Data Export to harmonize it with labels used in the API. Thereafter the labels in the API and Data Export will match. All used labels, including the label in our web user interface, will be made available through the legend to make cross-referencing easier.

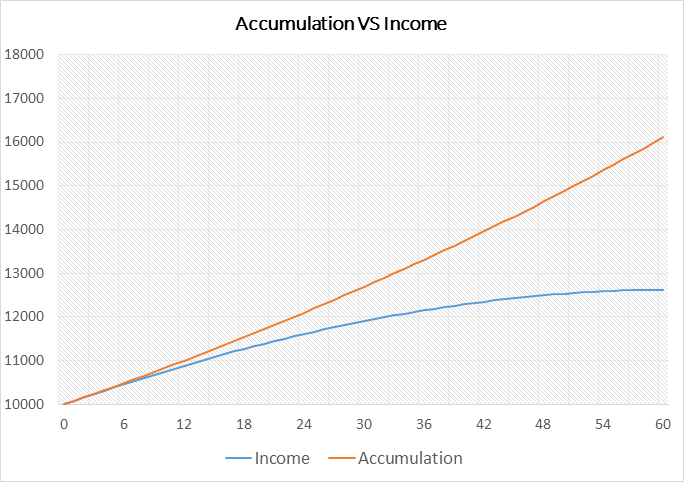

How to calculate net return?

Bondora use the XIRR function (extended internal rate of return) to calculate the net return. XIRR is used to return the internal rate of return for a schedule of cash flows that are neither necessarily periodic (payments are not made on a single day each month) nor always positive (portfolio has both outgoing and incoming payments).

Internal rate of return is a discount rate that makes the net present value (NPV) of all cash flows (repayments minus initial investment) from a particular portfolio equal to zero. Discounting cash flow means that you are reducing the future cash flow projections to arrive at its present value (how much 100 euro in a year from now is worth today). This is mathematically done by dividing the future cash flow by 1 plus internal rate of return in the power of the fractional period (e.g. if you are using an annual internal rate of return and a payment is 4 months from now then you would take 1 plus internal rate of return to the power of 4/12).

XIRR uses the loan issue date and amount, loan actual repayment dates and amounts and sum of scheduled future principal repayments (this is assumed by us to equal the present value of the portfolio) to calculate the internal rate of return of your investment portfolio on Bondora. This approach writes off all overdue and unpaid principal and interest payments immediately from the calculation. No assumptions for future interest payments or loss provisions are made as this is expected to be covered within our approach to arriving at the present value of the portfolio.

In other words, if you would borrow money at a rate equal to the net return shown on Bondora in order to finance your investments you would end up break-even. If you are borrowing money at a lower rate or your alternative investment opportunities (e.g. mutual fund) have a lower rate of return than you are making a profit compared to other options and it makes sense to continue or increase investment.

Can net returns of an outstanding portfolio change over time?

es, your net return over time can fluctuate based on the actual interest and principal repayments received. Overdue loans might start performing again and current ones become delayed. Recovery processes can take years to collect every penny owed, so even performance of very old portfolios might increase substantially over the years. Over time our servicing, collection and recovery practices are continuously improved and even higher risk portfolios can start behaving like lower risk ones.

Most of the fluctuations (calculated as the current net return vs. the net return calculated in the end of the specific calendar year) we have witnessed have been positive due to recovery efforts. Using data since 2012 there have been variances between -8.1% to +4.4%.

Can the net return calculation be improved?

Theoretically it would be possible to substitute the current present value sum of scheduled future principal repayments with the sum of actual discounted future cash-flows. However in order to accomplish this you would need to make a significant amount of assumptions about the timing and amount of the future cash flows from your outstanding portfolio. You would need to estimate when and how much would current loans repay and you would have to make the same assumption also for delinquent loans. Furthermore, you would need to discount these cash flows with a rate equal to actual XIRR of the fully matured investment or use future dates and payment amounts granularly in the model. In the end, one would simply arrive at a number based on a lot of assumptions that still needs to be tested in reality.

We have seen some investors build their own risk-adjusted models that simply take the outstanding principal balance and reduce this by a fraction of the overdue loans. Although this might at face-value seem like a reasonable step, it ignores the fact that outstanding loans will make both interest and principal repayments, as will recovered loans. This logic could be applied to investments with very low rates of return (where future interest payments are discounted to zero or to negative numbers) however not to consumer loans carrying reasonable risk-adjusted interest rates. In other words in case one would discount overdue loans at the same time performing loans would be taken into the present value with a premium.

In case you are interested in trying to establish a better model for calculating the present value then we recommend using the Historic payments and Future cash flows data exports under public or your personal data. Simply using outstanding amounts is not sufficient for building a model.

The enclosed file gives you a template example of discounting future cash flows and calculating XIRR at different points in time over the cycle of a portfolio. It also includes all the data used in the actual return calculations presented in the analyses above. Sheet ‘Xirr Calculator Example’ displays a basic model that includes some elements to include in your own analyses. Cells in yellow can be edited and white cells are fixed (please note that this example is for a 52 month term portfolio). Calculations related to ‘Bondora XIRR’ are based on the logic currently used on Bondora whilst ‘Perfect XIRR’ calculations are based on a situation where one would have perfect information available at any time during the cycle.

Can net returns be positive even in case default rate is above the interest rate?

Net returns on a portfolio can be substantial even if cumulative default rate is equal or even above the nominal interest rate. This is because the performing portfolio continues to generate interest and repayments over the full cycle of the loan not only in a single year.

Over an average 52 month cycle the performing loans and parts of the non-performing loans generate and pay interest for 52 months. Therefore in case one would want to compare this number with the cumulative default rate then the nominal rate should either be cumulated as well or the default rate annualized over the 52 month period. In the calculation model shared above we have built cash flows for an imaginative portfolio with 10% nominal interest rate and a 12% cumulative default rate to illustrate this.

We have seen some investors build analyses where portfolio returns have been calculated as interest rate less cumulative default rate (or cumulative expected loss). Furthermore some of these analysis have been done by calculating tax income on the nominal interest rate although non-performing loans do not pay interest and hence are not taxed. Such models unfortunately are misleading at best due to the reasons explained above.

Please make sure you use the full cash flows when building your own portfolio evaluation models and apply taxation only to actual paid interest not nominal values.

How are recovery rates measured?

Bondora calculate the recovery rate by comparing actual principal cash flow (net of write-offs) that occurred after the default with principal cash flow that we would have expected from the loan in case it had paid according to the agreed schedule. This measure allows us to determine the expected capital loss on loans that default.

Data is aggregated to larger cohorts and recent data are excluded as otherwise outliers will skew the results too much (e.g. 1 customer repaying the full amount after default at once). On the Bondora level this means excluding the last three months of defaults and using country based quarterly cohorts. Data on individual portfolios should likely be viewed on a higher level either using yearly country based cohorts or simply quarterly cohorts across all countries.

How to find recovery rates using Bondora statistics?

You can easily find information on recovery rates on the entire Bondora portfolio through the Recovery Rate chart on Public Statistics. The same chart is also available for the portfolio of each individual investor in your Personal Statistics page. Simply adjust the period, country, planned, actual and group by filters to pull out the data you want.

Some tips to help you master the Recovery rate chart:

- The period filter looks for loans that defaulted in the specific time range.

- The country filter allows to look at defaults from a specific country.

- The status filter segments the data based on the loans current status (Defaulted = loan is still in default; Full recovered = the loan has been repaid in full; Restructured = a new payment schedule has been agreed; Sold = loans you have sold – this is only applicable to your private portfolio).

- The recovery status filter allows you to analyze the performance based on the latest high-level collection and recovery stage assigned to the loan.

- Planned and actual filters make it possible to determine how the recovery rate is calculated. You can for example compare planned interest vs. actual interest received or planned principal vs. actual principal received.

How are investments taxed?

The profits earned through Bondora are in general taxed based on the gross interest received and the residency of the investor. Please declare interest income to your local authority in accordance with the law. Keep in mind that with peer-to-peer lending individuals generally cannot offset losses against income.

Please check with your local tax authority if, how and when you need to report your income.

To make the reporting easier for investors, we have prepared a Tax Report with the necessary information included. The report can be found on the Reports page on your Bondora account.

Consumer lending market in Europe

The European consumer credit market is the most relevant market for Bondora and its trends and developments will play a significant role in the success of Bondara’s business. The development of new technological solutions, changes in economic conditions, and the growth and acceptance of online lending are among the key driving factors that have reshaped the European consumer lending market. Bondora’s business model is designed to capitalize on these trends and developments.

The total market size of the European consumer credit was EUR 1.07 trillion in 2014; after reaching EUR 1.16 trillion in 2008, it contracted for five consecutive years. That said, the market appears to have stabilized; it experienced only a 0.3% year-on-year decline in 2014.[1] For 2015-16, expectations are for moderate growth overall, though with significant differences among individual countries in the region.

The European consumer credit market can generally be divided into three groups: Northern Europe, Continental and Southern Europe, and Eastern Europe.

Countries in Northern Europe, such as the UK, Ireland, Denmark, Finland, Norway, Sweden and Germany, have relatively high consumer credit penetration rates, with per capita volumes above EUR 2,500. Finland is positioned at the lower end of the spectrum; at EUR 2,563, per capita consumer credit is fairly modest when viewed from the perspective of its overall economy.

Per capita volumes are less than EUR 2,500 in the Continental and Southern European countries, which include France, Austria, Netherlands, Spain, Italy and Portugal, while the consumer credit market is least developed in Eastern Europe, where per capita volumes are less than EUR 1,000. The European Union average is EUR 2,100.

Recent market dynamics have contributed to variations among and within the three groups, with relatively faster growth being seen in several Eastern European countries, the UK, Finland and Sweden. In contrast, certain countries in Southern and Eastern Europe are experiencing declines.

Following the 2008 global financial crisis, the banking sector witnessed a shift in market dynamics, driven by increasing regulation (e.g., Basel III and CRD IV). The changes have forced banks to improve their balance sheets and focus on core products in domestic markets, and have led to an overall decline in the appetite for credit risk. Consequently, it has become harder for individuals to obtain credit from commercial banks. Because demand for consumer credit remains strong, many prospective borrowers have turned to non-traditional lenders.

The banks’ retreat from consumer lending and technological evolution have been driving forces behind the emergence of alternative lending models and new players. Digital channels offer opportunities to reduce costs and improve customer targeting, as well as the ability to capitalize on advanced scoring and underwriting methods.

As a result, digital lending has been a credit market game changer. Among the features that distinguish digital lending, which has an estimated addressable market of EUR 760 bn,[2] are new players offering a pure online experience, the ability to tap additional data sources when evaluating potential borrowers, and the ability to consolidate different aspects of lending.

Perceptions about non-traditional lenders have also been improving as they have sought to burnish their image and that of the sector. As they make inroads in presenting themselves as credible alternatives to traditional unsecured consumer lenders, and as banks continue to shift their focus from expansion to extracting value from existing customers, non-bank lending is expected to become an increasingly important aspect of the consumer lending business. The fact that banks in several markets have begun cooperating with new entrants by capitalizing on their technological advantages and financing loans underwritten by non-traditional lenders will likely bolster this trend.

Aided largely by expansive monetary policy in Europe, and in the eurozone in particular, economic growth and consumer confidence have been spending more time in positive territory in recent years, which should continue to spur moderate growth in the consumer lending market. The pace of expansion is expected to mirror that of the overall economy, and with the odds of an expansive credit boom appearing to be low, market dynamics should remain relatively healthy.

Europe’s evolving consumer lending landscape has led to additional regulatory scrutiny and altered perspectives on regulation in many countries. This stems from a desire to increase financial system stability at the time when non-traditional lenders are accounting for a large and growing share of credit activity and to ensure consumers are adequately protected. In light of this, the regulatory risks and other aspects of operating in this market are becoming much more important.

To succeed in such an environment, lenders must be able to adapt quickly to new regulations and changes in product offerings and requirements, and direct ever greater attention to the risk management and data-related issues that Bondora has been strongly focused on.

[1] Source: Overview of the European Consumer Credit Market, Credit Agricole, July 15, 2015

[2] Source: Digital Lending: The 100 Billion Dollar Question, Autonomous Research, January 2016.

General statistics on Bondora

- Average loan amount: 2500 EUR

- Average loan duration: 47 months

- Average interest rate: 31.9%

- Loans issued: 91.6 M EUR

- Net return: 14.6%